Digging Yourself Out of Debt

- T. Shepherd

- Jul 27, 2020

- 9 min read

Updated: Jul 31, 2020

!!!WARNING: This is a bit of a long-winded article but I am extremely passionate about this topic and to be honest, I could probably write an entire book on it, but I'll spare you the misery for now!!!

We are all born without a worry in the world or penny to our names, but soon find ourselves buried by mounds of suffocating debt. For most, it starts in the form of an auto loan when we get that little piece of plastic that grants us the ability to propel a ton of brand new metal 80 mph down the freeway. It doesn't stop there either. The next step is to get the harder piece of plastic so we can start "building credit" to one day move out of our parents and into a sweet place of our own. Then before we can even walk across the stage with our high school degree, we have already shackled ourselves to tens of thousands of dollars to chase another.

If you're one of the roughly 35% people who actually completes college with their bachelors degree and can swing a gig that pulls in enough dough to start paying back the growing hill of debt, the next logical step is to pile on even more in the form of a mortgage. You can't have a new place without accouterments, so let's go out and put some new furniture and appliances on a 12-month zero interest Home Depot credit card. Oh, and that brand new car you bought when you were 16 is now a relic, so it's probably time for you to buy a brand new one with all that hard earned and well deserved grownup job money! These are all natural parts of growing up in America but by now you can see how the average American finds themselves in $90,000 of consumer debt.

This can be a daunting mountain to conquer and will drive many to succumb to the temptation to continue to, as Dave Ramsey** would say "be a slave to the lender" and pay minimum payments for the rest of their lives. It's easy to fall into a giant grave-sized hole of debt but it's not always as easy to dig yourself out without the proper tools. One of the best tools you have in this battle is your income shovel, but no shovel is useful without a handle, and this handle comes in the form of a well-organized budget. Getting my budget together and sticking to it religiously was the turning point that propelled me on my journey to financial freedom.

So, with no further ado, here are the do's and don'ts that I learning from creating and leveraging a budget to get out of debt:

Technology can be your friend-- It's folktale that before the advent of computers and the internet, people would use archaic tools called spreadsheets in which they would manually balance their budgets and track spending. Luckily, we live in a day-and-age where, not only, is there a technical solution for almost any of our day-to-day problems, but there is almost always a free version that has 95% of all the functional you need to get value out of them. I say that technology "can" be your friend because if you're anything like me, you can find yourself lost in all of the bells and whistles and never find the true value lurking just below the surface. There are many different budgeting websites and services, but the one that I've stuck with the longest is Mint.com*. Mint allows you to plug in all your accounts, as securely as any site can, and automatically pull in all of your spending and account balances. They make it easy to set up and maintain your budget and even go the extra mile to take a stab at which category to assign to your transactions. They don't always get it right but it's a great head start to something that you should already be looking at frequently. I could, and may, do a completely separate post on the pros and cons of Mint, but I'll leave the suggestion here for you to take as you will for now.

Start small-- Just the word "Budget" is enough to send some into a panic attack, so trying to tell someone that they have to track everything they have ever spent is not realistic, nor should it be. The old adage "one is a chance, two is a coincidence, and three is a pattern" holds true for setting up your budget. You will want to use your last three months of transactions to establish your current spending patterns when first creating your budget categories. Your past is not indicative of your future, but it sure does give you one hell of a starting point! Once you have chosen your method of creating and tracking your budget, it's time to start categorizing those previous transactions. I know this task can sound extremely daunting at first, especially if you are currently a big spender, but it helps to just embrace the suck at first and break out your favorite adult beverage or dessert and make a night of it. Once you have assigned categories to all your purchase, you can now aggregate them and get a feel for your average spending in a given category. This will be your starting point for your ongoing budget.

Be realistic-- When I first created my budget and found my average spending per category, I was shocked at where all my money was going. This lead to an extreme adverse reaction of cutting each category to almost nothing, which just ended up placing more stress on the process and caused me to avoid my budget in hopes that all the red wasn't there. Keep the following tips in mind when identifying the initial budget amount for each category:

Find categories that you can live without. The most rewarding part of setting up my budget was being able to realize where I was spending money that I could go without and then whipping out that category all together. That extra money went into the "left over" bucket that could be allocated towards my goals. Worst case scenario is that you see it pop back up consistently month-over-month and you find room in your budget to add it back in.

Leave the rest of the categories alone for the first month or two. The first few months are your time to get familiar with the process and get an idea on what to look for and how you're spending lines up with your patterns. As you start to get an idea of where you are spending your money, you can start to adjust your spending behaviors to line up more closely with your saving goals.

Consolidate to broad categories-- As you start to track your spending, you will find that there is an almost endless amount of categories for the same general theme. For example, if I purchase a sandwich at the local sandwich shop, I could categorize it as "Fast Food", "Restaurant", "Groceries", "Eating Out", or "Food." You can see how this can prevent you front getting a full picture of where your money is going. I've found it easier to understand my spending when I come up with one category for anything that may be similar. So for me, a sandwich, no matter if it's from a fast food joint or a sit down restaurant or the grocery store, is categorized as "Eating Out." Now if I bought that same sandwich along with other groceries, I would just lump it into "Groceries." Budgeting is more of an art than a science so try to paint the picture rather than plot the points. My current budget*** has the following categories (largest to smallest allocation) in which all my transactions will fit into. There are occasions that I will buy something that doesn't necessary fit into one of these buckets but those normally find their way to the "Shit Happens" bucket.

Mortgage & Rent - My monthly home rental payment

Groceries - Anything I buy at the grocery story or Target*

Eating Out - All food that doesn't fall into the "Groceries" bucket

Amusement - Anything fun (e.g. poker night with the friends (hopefully it comes in as a credit and not a debt), AirBNB*, golf, random items that support my hobbies, movies, etc.)

Shit Happens - Anything that is unexpected (e.g. parking tickets, flat tire, lose the garage remote to the old house so I need to replace it before they can charge 4x the price I could get it at the hardware store, etc.) If I'm lucky, nothing falls into this bucket by the end of the month, but if small unforeseen things do arise, as they always will, I have that allocated amount to soften the blow of these unfortunate events.

Clothing - Anything that I wear. (i.e. shirts and pants, FitBit*, mountain biking gloves and sunglasses, etc.)

Alcohol & Bars - Booze! Whether I enjoy it at the bar, at home, at the park, or at the bottom of the slopes, it goes into my belly and into this bucket. This has gone down as I, and my maturity, have aged.

Gas & Fuel - Vehicle go-go juice. This will also include any amount I chip in for carpooling road trips. Be careful about items you buy inside the gas station falling in this bucket when they should really go to "Eating Out" or the actual category that they fit into.

Hair - Hair cuts and products

Rental Car & Taxi - Ubers* and Lyfts*

Mobile Phone - Monthly cellular plan bill. If you have a payment on your phone (which I hope you don't) it could also be lumped into this same category.

Utilities - Water, gas, garbage, sewage, and any other utilities you pay to live in your city.

Service & Parts - Small maintenance for your vehicle (e.g. oil changes, new wipers, wiper fluid, car washes, etc.) Now, if you know you will need a new set of tires in 20,000 miles, that would be a goal and not show up as a $700 transaction in this $20 monthly bucket. Also, if your radiator goes out, you could make the argument that it fits in this category, but I feel a little better categorizing that as "Shit Happens" so I can know that it was a hopeful rarity.

Music - For me, and probably a majority of others, this is to pay my monthly subscription fee to my preferred music streaming platform, Spotify*. If you are a vinyl head and buy vinyl every month, you would probably also want to place those purchase here.

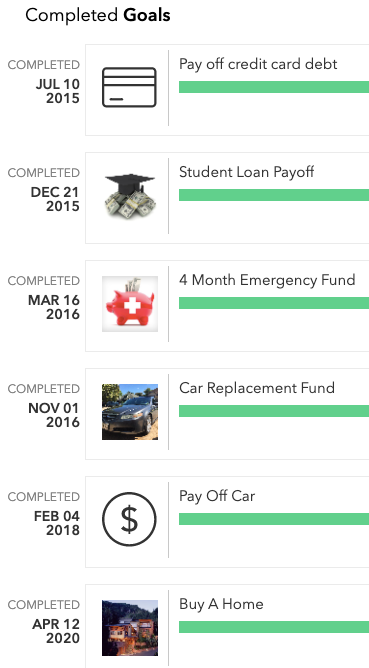

Set goals-- The whole point of a budget is for you to be accountable for what you spend so that you can have money left over to invest in yourself and your future. The best way to ensure that this effort is not in vain is to set and track your financial goals. This helps you allocate left over income each month to what is important to you and your future. This could be something as simple as saving for the latest iPhone* that you will die if you don't have come September to something as complex and seemingly insurmountable as saving for retirement. I find that having a visual progress indicator, as well as a picture to represent the end goal, helps me stay on track and try to beat the deadline. My current allocation of left over funds are going towards a car replacement fund**, which will be ongoing for the rest of my life as I know I will need a new used car every 3-5 years. You can also see my completed goals below**.

Frequency builds habits and habits breed success-- Budgets are not meant to be a means to an end but the process for financial success for the rest of your life. It's true that once you have been in the routine of managing your budget for an extended period of time, the frequency that you look at it will naturally subside. This is because you will have built the muscle and will now be in maintenance mode. I strongly suggest that you categorize each transaction daily and balance your categories and amounts at the end of each month for the first few months. Once you've laid the framework for your categories and have all your goals established, you can dial it back to reviewing your transaction categorization once a week and periodically reviewing and tweaking your budget category amounts. It's important to build up the habit of keeping your budget up-to-date and being cautious of where you stand throughout the month to have the positive benefits that a well organized and efficient budget can provide.

Conclusion-- Budgets can be scary and even boring at first, but if you stick with it, they can also be your most powerful tool in digging yourself out of debt and into financial freedom!

*I am not affiliated with Mint.com, Spotify, Target, Dave Ramsey, Apple, FitBit, AirBNB, Uber, or Lyft and only mentioned them by name because I use and enjoy their products and services.

**Below are screenshots of my completed and current goals from Mint:

***Below is as screen shot of my current budget categories from Mint:

Comments